- 1 Introduction to Stable Value Funds ›

- 2 Key Terms for Stable Value ›

- 3 The Stable Value Industry ›

- 4 Operational Nuances with Stable Value ›

- 5 Final Exam

Introduction to Stable Value Funds

On this page

Learning Outcomes

Executive Summary: This section is designed to provide learners with an introduction to stable value funds, including their purpose in preserving capital and offering modest returns. Learners will understand the investment strategies employed in stable value funds, the various types of contracts that ensure principal protection, and the risks inherent to these investment vehicles.

Learners will:

- Define stable value funds and explain their principal preservation and modest return characteristics.

- Learn the typical investment portfolio of stable value funds, including the role of government and corporate bonds, and differentiate between traditional GICs and synthetic GICs, also known as book value wrap contracts.

- Identify and discuss the various risks associated with stable value funds, including fixed-income risk, cash flow risk, contract risk, event risk, and the impact of inflation.

- Explore the mechanisms in place to protect investors in stable value funds, such as investment contracts ("wraps"), and how they function during market volatility to provide stable returns.

What are Stable Value Funds?

A stable value fund is a type of investment only available in the US that protects investment principal while providing steady interest income normally at a rate above cash equivalent investments without a significant increase in risk. Stable value fund characteristics include:

- Protection: Protects investors from capital loss using an investment contract offered by either an insurance company or a bank.

- Steady returns: Provides gradually changing steady returns over time.

- Low risk: Preserves principal and minimizes risk.

- Diversification: Provides diversity to a defined contribution plan's asset allocation.

- Liquidity: Provides a high degree of liquidity to allow investors to contribute to or withdraw from the investment on a daily basis.

Stable value funds are not traded on the market and are only available as part of retirement defined contribution plans set up by employer sponsors.

Stable value is a unique investment product, which can only be offered in tax-qualified, defined contribution plans, such as 401(k), 401(a), 403(b), and 457 plans, and some 529 education savings plans and healthcare savings plans. These products are subject to insurance and banking laws, accounting rules under the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB), and may also be subject to the Employee Retirement Income Security Act (ERISA).

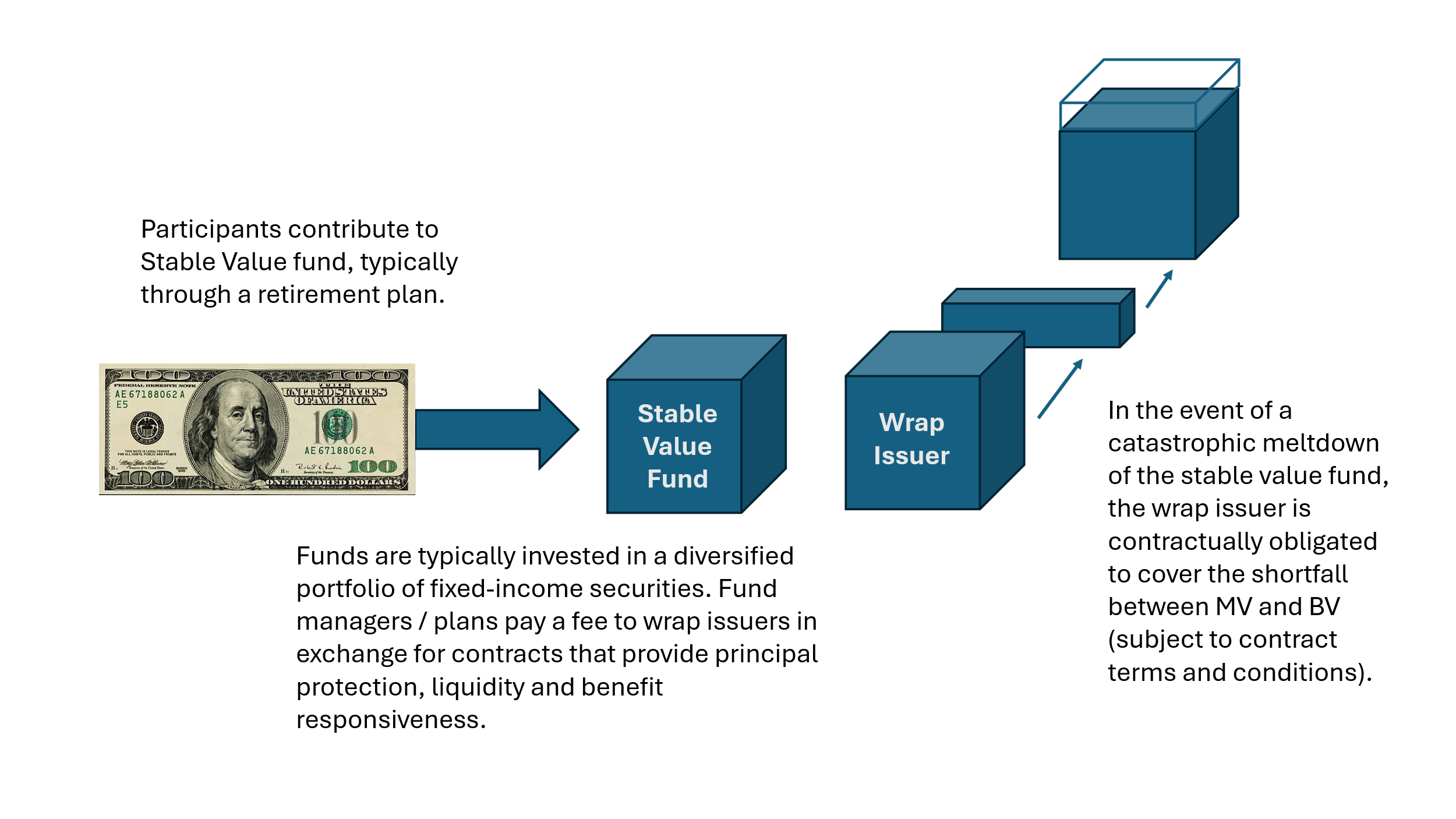

Stable value products protect investment principal while avoiding daily market fluctuations, offering stable returns and easy access to funds. To provide these advantages, stable value products often use various types of investment contracts issued by creditworthy insurance companies or banks. These contracts guarantee participants a minimum interest rate of at least 0%. As a result, participants can withdraw or transact based on the book value of the contract (their deposits plus any earned interest), instead of the fluctuating market value of the assets.

Stable value funds provide similar principal preservation as a money market fund, while historically producing slightly higher returns. They provide short-to-intermediate maturity bond-like returns with low volatility, which can provide investors with an attractive risk/return profile. Like a bond fund, stable value products take advantage of the term premium, credit and convexity risk premiums, and the spread differential over similar-duration U.S. Treasury bonds. Unlike bond funds, stable value products offer day-to-day principal preservation via the contractually set crediting rates provided by the stable value contracts.

Stable value funds usually invest in high-quality bonds, including government or corporate bonds, short-term bonds, and intermediate-term bonds. They may also invest in other stable value instruments such as guaranteed investment contracts (GICs), alternatives, collective funds, or mutual funds. Common stock may sometimes be used for a small allocation with contract issuer approval.

In the highly unlikely event that the portfolio's market value is less than the book value of the contract and all participants request benefit payments at the same time, the underlying bonds will be sold for cash to cover the payments. If all the bonds have been sold and additional benefit payments are requested, only then will the insurance company (or bank) that offered the stable value contract make a payment into the stable value fund for those remaining participant benefit payments. It should be noted that both the contract issuer and the stable value managers would work together to avoid this scenario and that multiple steps and negotiations would take place before any fund liquidation and contract issuer payment would occur.

Types of Stable Value Funds

There are three main types of stable value contracts: (i) traditional guaranteed investment contract (GIC), (ii) synthetic guaranteed investment contract or book value wrap contract (SynGIC, SGIC, or wrap), and (iii) separate account contract. All contracts are a hybrid mix of an investment security (or securities) and a bank investment contract or life insurance contract.

Traditional Guaranteed Investment Contract (GIC)

A traditional GIC is issued by an insurance company or its affiliate and is backed by the company's assets in its general account. The buyer, also known as the contract holder, agrees to deposit money with the insurer until a maturity date, and in exchange, the insurer promises to pay the investor a certain rate of interest and return the principal at maturity.

The terms for a GIC include a deposit amount with an annual interest rate and one or more maturity dates. Modeling details are similar to bonds and include compound frequency, interest payment frequency, day counts, etc. Typically, a GIC has a fixed rate, but it can have a variable or floating rate. Traditional GICs are often referred to as non-participating or non-par contracts because the contract's fixed rate is not affected by the contract's cash flow experience or the performance of the associated assets.

The GIC is benefit-responsive, which means that plan participants may withdraw assets from the GIC at their book value (i.e., their deposits plus accrued income), even if the insurance company investment assets backing the contract have decreased in value.

GIC issuers make money through the spread they earn from the yield of the insurance company general account investments, and any underlying fees are not disclosed to the buyer.

Synthetic GIC or Book Value Wrap

A synthetic GIC or book value wrap is a stable value investment contract that offers similar characteristics as a traditional GIC (e.g., pays a specified rate of return for a specific period of time and is benefit-responsive). Unlike the traditional GIC, a synthetic GIC contract's rate of return (or crediting rate) is calculated on a monthly, quarterly, or sometimes even yearly basis and is based on a formula which incorporates the yield of the underlying bond portfolio, market value of the bonds, book value of the contract, duration of the underlying bond portfolio and typically fees on the contract. Also, unlike the traditional GIC, any gains or losses in the portfolio flow through the crediting rate formula and are passed on to the participants with the stipulation that the crediting rate can never be less than 0%. This is why synthetic GICs are typically referred to as "participating" contracts as they participate in the underlying wrapped bond portfolio's performance. A synthetic GIC includes an asset ownership component, and a contractual component that provides for participant book value benefit payments, even if the value of the assets has decreased.

The stable value manager manages the assets as a short-to-intermediate fixed-income portfolio and the underlying characteristics of the portfolio determine the rate of return on the book value. The associated assets backing the contract's book value are owned and held in the name of the plan by the plan's trustee. As deposits and withdrawals are made by plan participants, the transactions generally occur at the participants' stated book value with limited exceptions.

The underlying assets typically consist of a diversified fixed-income portfolio, including but not limited to treasury, government, mortgage, and/or corporate securities of high average credit quality. When participants make withdrawals from the stable value fund, the stable value manager relies on the assets within the fixed-income portfolio, generally beginning with short-term securities known as the cash buffer. This position is predetermined by the stable value manager and the contract issuer to cover benefit-responsive payments to participants. As the cash buffer is depleted, it is replenished with either cash flows from the fund's assets, new participant deposits, or from selling assets in the fund. In the extremely unlikely scenario that the fund's assets could not cover benefit-responsive payments to its participants, the stable value contract would be enacted and the financial institution insuring the fund's principal would be required to cover the difference between the fund's market value and the book value owed to investors.

This is a highly simplified version of how the stable value contract would cover the difference between the market value of the assets and the book value of the contract and is not a routine occurrence, as the cashflows of the portfolio are typically available to cover any participant benefit payments. Additionally, there are multiple contractual protections that would require certain actions be taken by the stable value manager to protect the stable value fund should participant outflows begin to rise at a concerning rate. To be clear, a payment by the contract issuer to cover the difference between the market value of the assets and book value owed to participants would only be needed if participant withdrawals exceed the available market value when the market value is less than the book value.

The terms for a synthetic GIC include an initial contract amount, rate reset terms, modeling details, termination events, market value events, and investment guidelines for the fixed-income holdings. Investment guidelines may include limitations based on sector, ratings, duration, and how to manage an asset if it is impaired. There is no contract maturity date, thus these contracts are typically referred to as "evergreen."

The investor (in wrap terminology, this would be "the contract holder") may terminate the contract at market value with proper notice at any time, or at book value if market value is above book value. Contract terms determine how the contract will terminate. If market value is below book value the investor may still terminate the contract, but the difference between the market value of the assets and book value owed to participants is not paid. In most cases, the contract issuer can only terminate the contract through the extended termination (i.e., immunization) process, otherwise the contract remains evergreen. The extended termination process allows time for the market value to increase to equal the book value before the contract terminates, which protects the participants from experiencing a market value loss. In addition, in the event of an extended termination, replacement guidelines will apply that shorten duration and move the portfolio to more conservative assets. These guidelines typically apply 12 months after the immunization date.

Synthetic GICs provide a rate of return. The rate is defined by one of several industry formulas using market value, book value, duration, (possibly a duration adjustment factor) and yield. Here are example crediting rate reset formulas:

Crediting Rate = Y + (MV - BV) / (BV * D * DAF) - Fees - Other

Crediting Rate = Y + (MV - BV) / (MV * D * DAF) - Fees - Other

Crediting Rate = (1 + Y) * (MV / BV) ^ (1 / (D * DAF)) - 1 - Fees - Other

To learn more about synthetic GIC mechanics explore our crediting rate training tool.

Synthetic GIC issuers make money through daily fees accrued based on the book value. Fees vary but may be approximately 15 basis points (bps) for a standard wrap contract. Fees may vary depending on several factors including: product type (pooled fund or individually managed fund), plan type, perceived underlying risk of the plan, and the complexity of the contract terms and underlying assets being wrapped.

Insurance Company Separate Accounts

An insurance company separate account is a stable value investment option entirely offered and guaranteed by a single insurance company, with the underlying assets typically managed by the insurance company or an affiliated investment manager. It is the responsibility of the plan sponsor to select the stable value solution that best fits the needs of their plan. Separate accounts may be set up for one plan or may allow many plans to commingle their assets. Separate account products are generally viewed as a safer option in the event of an insurance company liquidation scenario, as assets are held separately from the general account specifically for the benefit of the plan participants rather than being pari passu with other policyholders. Separate accounts may come in various "flavors." Crediting rate may be fixed or formulaic and tied to an index or performance of the underlying assets. Separate accounts may have specific investment guidelines and in some cases can be slightly more aggressive. Term may be fixed or evergreen. The account may charge fees which are contractually specified.

Investment Vehicles

Individually Managed Funds

A stable value investment option in which the assets are owned by and managed for a specific plan's participants. These accounts are usually managed by an independent investment management firm or by employees or affiliates of the plan sponsor. Individually managed funds allow for a higher degree of customization than other stable value investment options. These accounts are generally only available to plans with substantial stable value assets, however, minimum account size varies by firm.

Pooled Funds / CITs

Also known as collective investment trusts (CITs). These funds combine the assets of unaffiliated plans into one commingled fund. Pooled funds are generally used by plans that don't meet the minimum size for an individually managed account or do not require plan specific customization. With respect to a stable value investment option that is a commingled fund, the fund purchases stable value investment contracts and other investments on behalf of the invested, unaffiliated plans.

In many cases, contract issuers consider pooled funds to be relatively low risk because of the typically large number and diversity of plans participating in the fund. Additionally, because discretion over the assets is not isolated to a central decision-maker and benefit-responsive withdrawals must be initiated at the participant level, the underwriting of the fund assumes the entire pool will not initiate withdrawals all at once. The stable value contract issuers normally require the pooled fund to require 12-month written notice for a plan sponsor to withdraw any or all assets from the pooled fund at book value.

Risks Mitigated with Stable Value Funds

Sequence-of-returns risk refers to the danger that a sharp drop in the market value of risky investments happens early in retirement. When retirees regularly withdraw from their portfolios during this time, they may end up selling these investments at low prices, locking in significant losses. Even if the market improves later, the portfolio can be quickly drained.

To help protect against this risk and increase the chances that a portfolio lasts throughout retirement, one approach is to start with a more conservative investment strategy and gradually take on more risk as retirement progresses. A straightforward way to do this is by setting aside enough money to cover several years of withdrawals in a low-risk investment, while investing the rest more aggressively. Withdrawals would then come from the low-risk portion, allowing the riskier assets to grow for years. This strategy, known as a "bond tent," involves increasing the allocation to low-risk assets before retirement, peaking at retirement, and then tapering off, creating a triangular shape that resembles a tent. The stable value fund can provide the low-risk portion of the participant's assets.

Knowledge Check

0 of 7 answeredAnswer all 7 questions to mark this section complete.

What is the main objective of stable value funds?

Stable value funds are only offered in which of the following?

Which of the following is a typical underlying investment of stable value funds?

What type of contract is typically used to provide a guarantee of principal in stable value funds?

How do stable value funds generally perform during market volatility?

What is a potential disadvantage of investing in a stable value fund?

Why might an investor choose a stable value fund over a money market fund?

Feedback and suggestions are welcome at info@stablevalue.org.